Uganda’s current economic architecture is rooted strongly in the sweeping structural adjustment and privatization policies of the 1990s. These were initiated to dismantle inefficient state-owned monopolies, foster private sector-led growth, and integrate the domestic economy into regional markets. The privatisation journey was fundamentally designed to introduce robust competitive mechanisms, following the classical liberal economic theory, in which competition is championed as a self-regulating force that optimizes consumer welfare, drives downward pressure on prices, and incentivises firm innovation.

Indeed, private sector investment has grown to about 80% of the GDP as of 2026, expected to grow even further to about 90% by 2040, according to National Development Plan (NDP) IV. However, as markets expand, the structural framework ought to ensure that competition remains fair, transparent, and symmetric lest it deviate from a healthy mechanism of productivity into an existential, structural barrier, especially for legally registered and fiscally compliant enterprises.

This blog uses the Economic Policy Research Centre’s (EPRC) quarterly Business Climate Index (BCI) reports to examine the evolution of competition in Uganda’s market. Since BCI’s inception in 2012, firms have flagged competition as a major constraint to doing business, and it has gradually evolved from a standard race for market share to a complex, unfair playing field.

The Jan-march 2025 BCI report flagged a massive surge in increased competition from fellow businesses, which rose to 15.9 percent, emerging as the second most critical business constraint. The constraint evolution index confirmed that 32.1 percent of firms experienced worsening competitive conditions. The report explicitly linked this spike to unregulated retail entry, highlighting how the opening of the massive, foreign-owned China Town Super Store in the Kampala retail market triggered a severe business outcry due to hyper-cheap pricing structures that immediately drew away local customer bases.

During the April-June 2025 quarter, competition from other businesses rose to 19.8 percent of total constraints, with an overwhelming 62.8 percent of firms stating that the constraint was actively worsening. Crucially, the evolution index tracked a massive 50.3 percent spike in the severity of competition from substandard products.

The BCI report explicitly warned that these cheap, substandard, and counterfeit imports were actively undermining quality-conscious businesses and eroding consumer trust. As a result, firms adhering to standard compliance were forced into margin compression because they couldn’t match the rock-bottom pricing of substandard goods.

By FY 2025/26, competition evolved from product quality distortions to absolute asymmetric regulation, forcing the EPRC to modify its metrics to isolate competition from informal firms. During the Jul-Sept 2025 BCI survey, firms identified an overwhelming combination of systemic blocks, i.e., multiple taxation at 77.24 percent and competition from informal businesses at 68.37 percent. The constraint evolution metrics recorded worsening multiple taxation and unfair competition from informal firms at 21.4 percent and 16.5 percent, respectively. Informal enterprises operate completely outside the state’s regulatory and tax nets and face no overhead costs borne by registered corporations. Consequently, informal firms heavily undercut formal prices, trapping law-abiding businesses in an unviable environment.

This destructive dynamic hardened during the second quarter of 2025/26, as taxation and competition from informal firms remained the most severe constraints, at 18.7 percent and 17.3 percent, respectively. Over 64.6 percent of firms stated that informal undercutting had worsened, a crisis compounded by the fact that formal firms were simultaneously absorbing the massive operational disruptions of the April 1, 2025, electricity transition from UMEME to UEDCL, which induced severe power outages for 73.7 percent of affected firms.

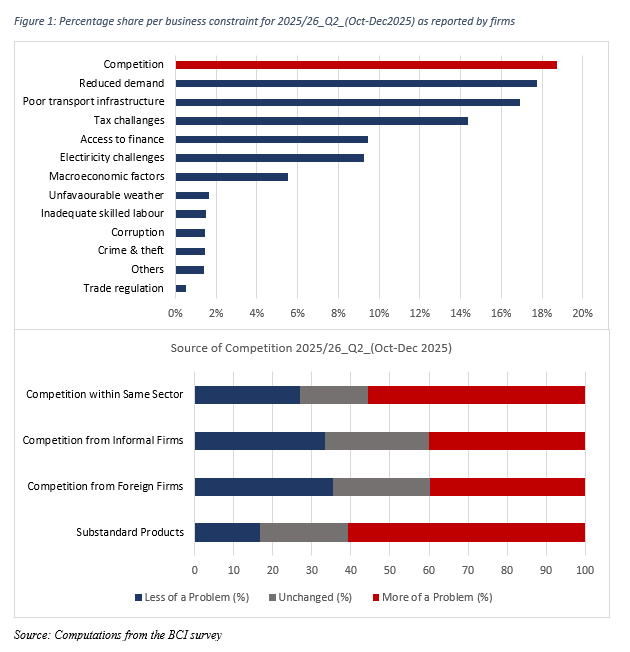

The Oct-Dec 2025 BCI survey officially reported competition as the single highest share of business concerns at 19 percent, eclipsing reduced demand at 18 percent and poor transport infrastructure at 17 percent. A deep look into the competitive dynamics during this second quarter reveals that this stress was heavily driven by the persistent vulnerability to substandard products, which 60.65 percent of firms reported as an intensifying problem, alongside a 55.66 percent surge in worsening competition within the same sector.

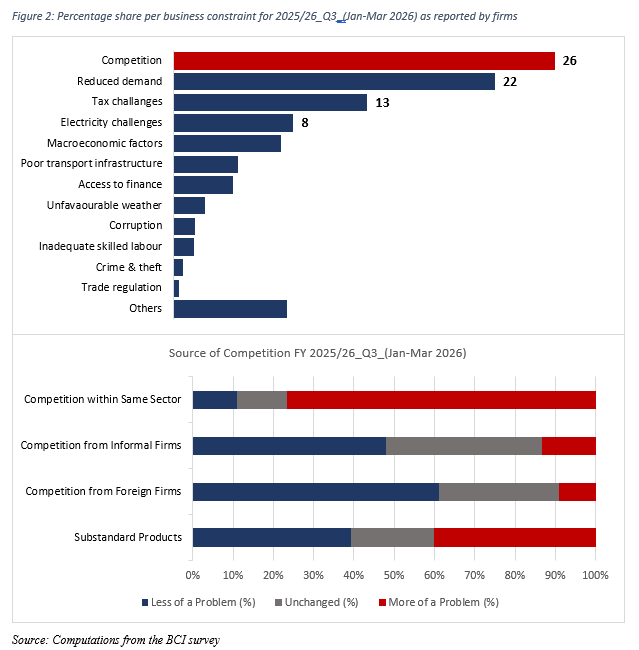

The most recent Jan-Mar 2026 Q3_BCI survey, as shown above, still reports that competition expanded its grip to capture a staggering 26 percent of all business challenges, relative to reduced demand at 22 percent and tax challenges at 13 percent. Crucially, 76.54 percent of businesses reported that competition within their same sector had become significantly more of a problem, even as substandard goods and informal firm pressures persisted.

During recent direct firm engagements, formal retailers expressed deep distress over strategic encroachment by manufacturers and wholesalers who bypass traditional channels to sell directly to end-consumers at wholesale rates. This structural disruption is aggressively compounded by highly mobile, informal operators utilizing lorries and ‘tuku-tukus’ that run unlicensed pop-up shops, completely untethered from the overhead burdens of commercial rent, municipal licensing fees, or formal tax levies. These mobile traders leverage a low-cost operational structure to command an artificial, asymmetric pricing edge that compliant retail enterprises cannot legally match.

Conclusion

While competition is desirable for efficient market outcomes, evidence shows that markets that are characterized by severe distortions, including information asymmetry, uneven regulatory enforcement, inflows of cheap substandard goods, aggressive price undercutting by informal non-compliant enterprises, and multiple taxation on registered firms, create a destructive race to the bottom where competition penalizes compliance and quality instead of rewarding productivity. These pressures compress profit margins, discourage investment, weaken dynamic efficiency, and drive the premature collapse of formal businesses.

The current regulatory framework remains ineffective because the Competition Act, 2023, primarily targets formal corporate indicators such as audited turnover and asset control, leaving informal actors largely outside enforcement, while institutional fragmentation between the Ministry of Trade, Industry, and Cooperatives (MTIC) and the Uganda National Bureau of Standards (UNBS) disconnects antitrust enforcement from product quality control.

The evidence, therefore, points to the need for a single autonomous competition and markets authority that integrates antitrust enforcement with strict quality certification and incentives for business formalisation to restore fair competition, protect productive enterprises, consumer welfare, and support long-term economic growth and development.